.jpg) Nicholas Lamparelli

Nicholas Lamparelli

3 min read

Becoming a Trusted Advisor in Catastrophe-Prone Areas: A Guide for Insurance Agents

I recently had the opportunity to present to several dozen agents for the PIA Western Alliance last week. The title of my presentation was: ”Wildfire...

3 min read

I recently had the opportunity to present to several dozen agents for the PIA Western Alliance last week. The title of my presentation was: ”Wildfire...

3 min read

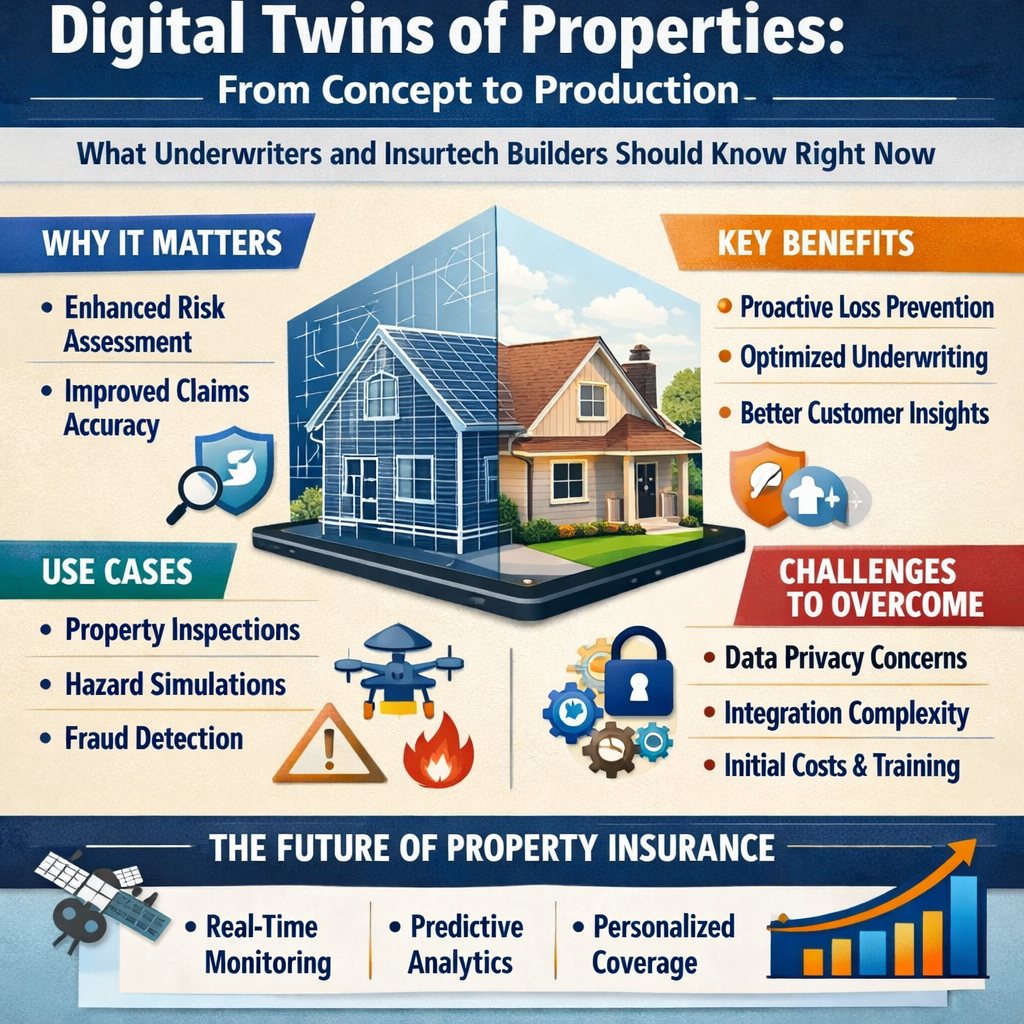

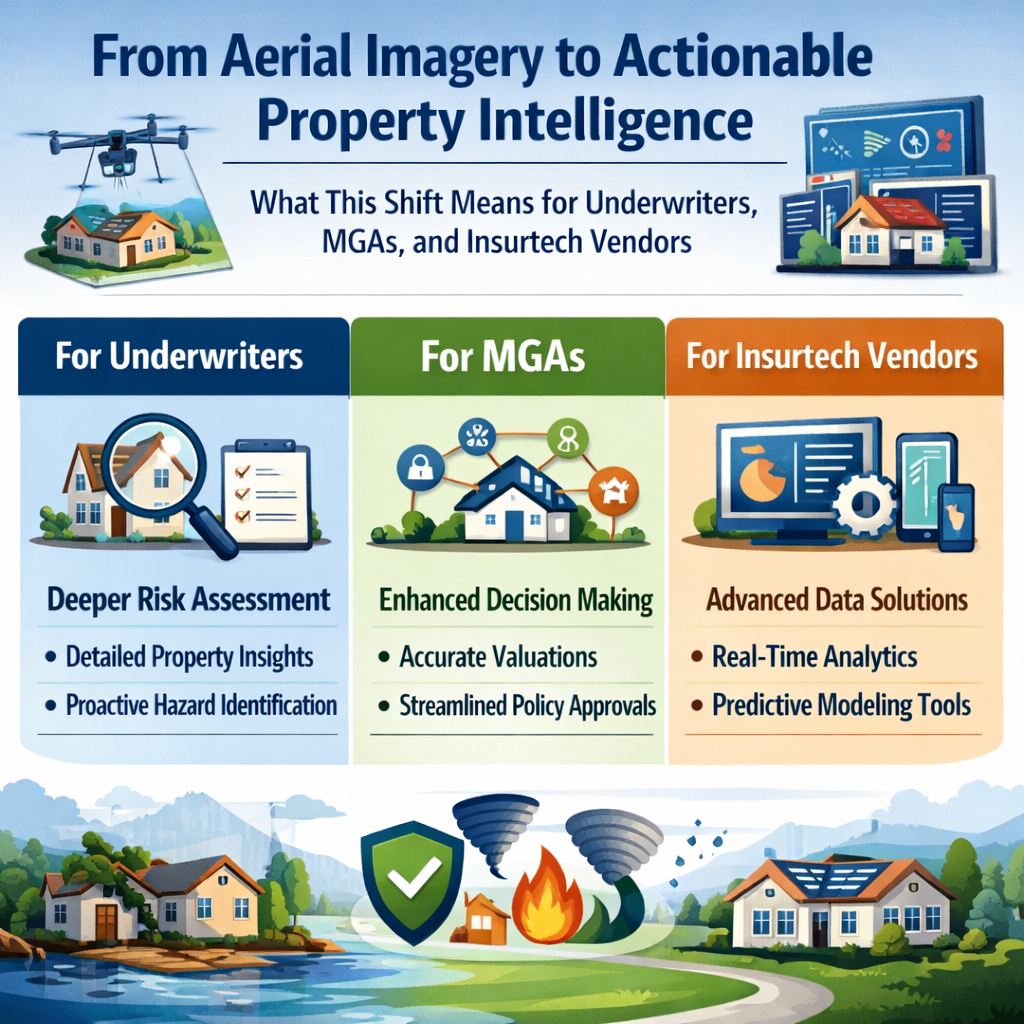

The market for geospatial property data is shifting from raw imagery to pre-digested, decision-ready analytics, and the implications ripple across...

2 min read

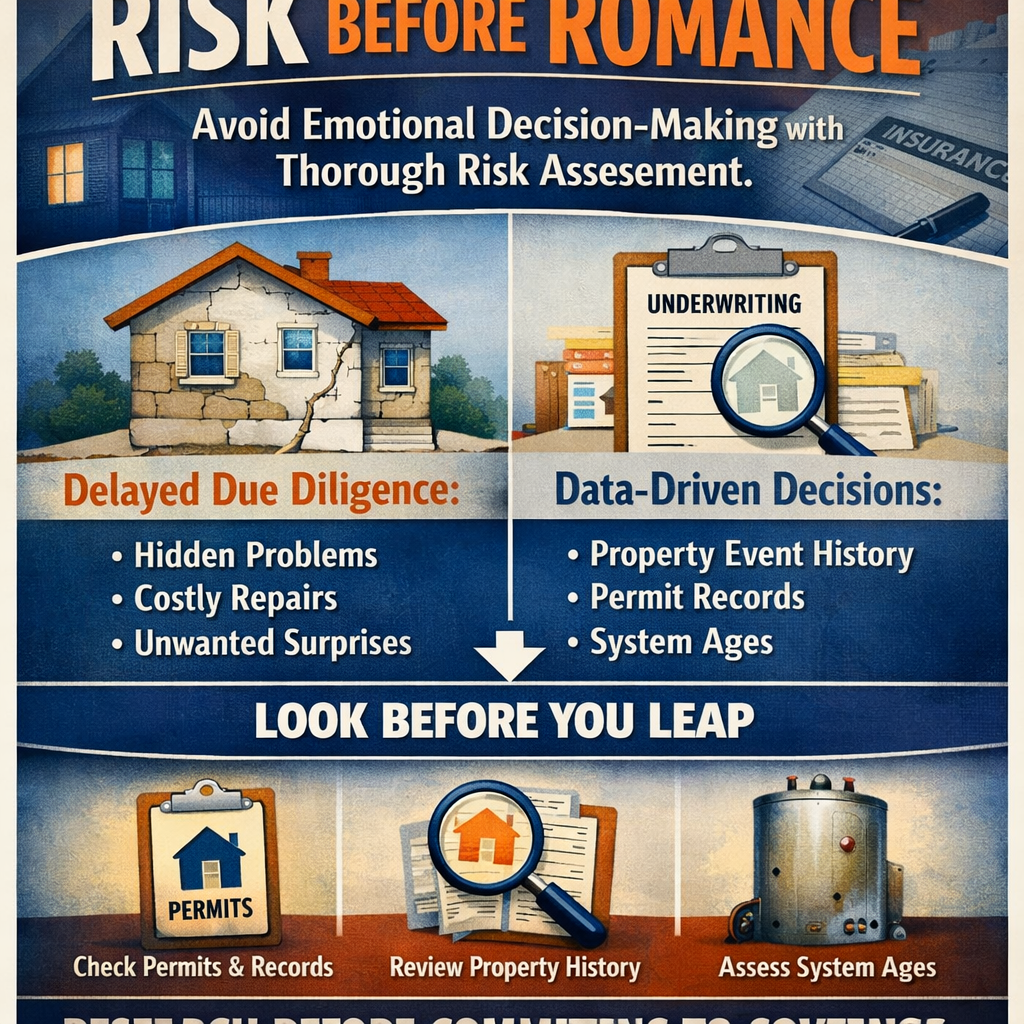

A PropertyLens article exploring homebuyer decision-making reveals a principle that resonates directly with insurance professionals: thorough risk...