Michelle Bothe

Michelle Bothe

3 min read

Becoming a Trusted Advisor in Catastrophe-Prone Areas: A Guide for Insurance Agents

I recently had the opportunity to present to several dozen agents for the PIA Western Alliance last week. The title of my presentation was: ”Wildfire...

By 2025, geocoding accuracy stopped being marketed as a background feature and started showing up as a primary product differentiator.

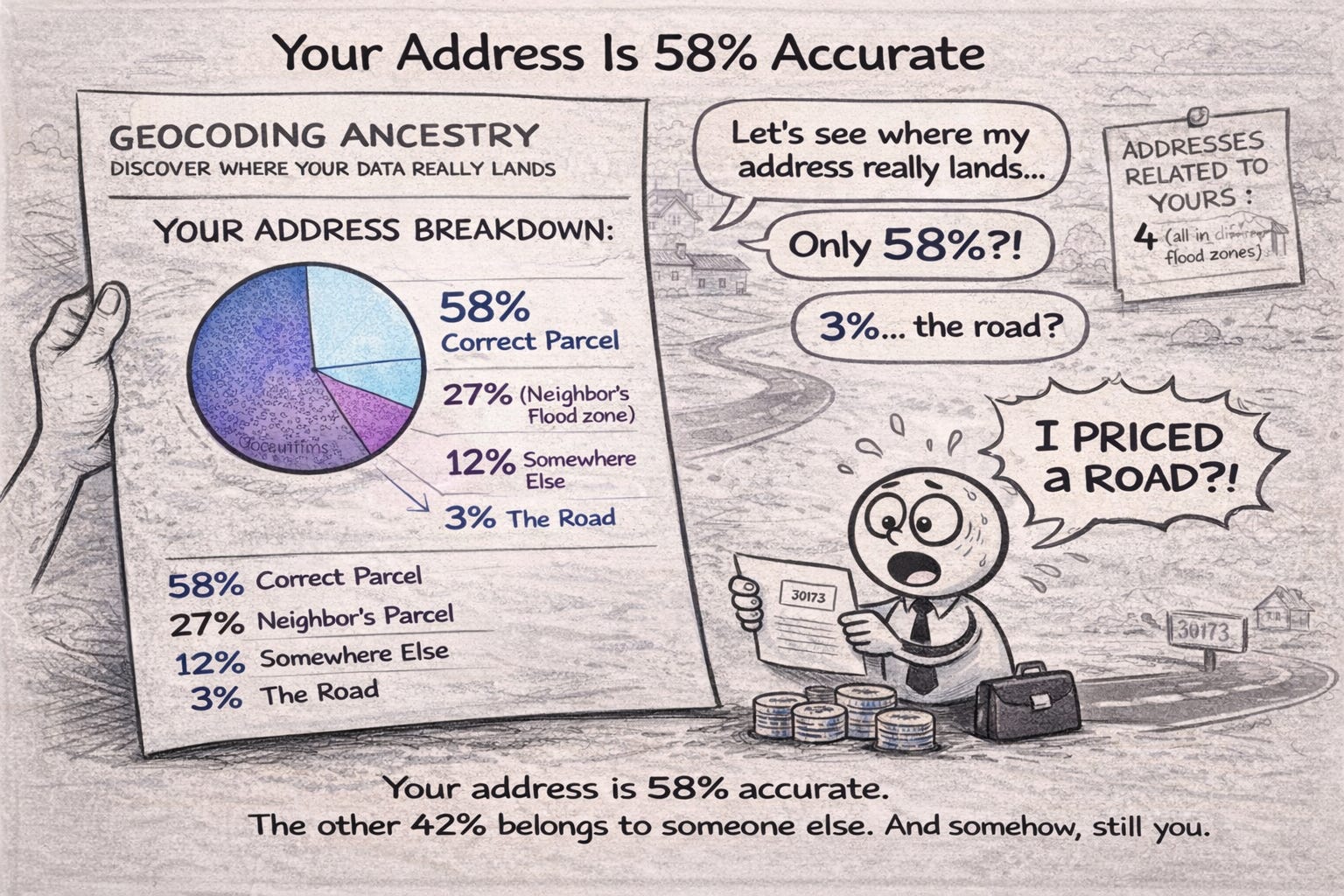

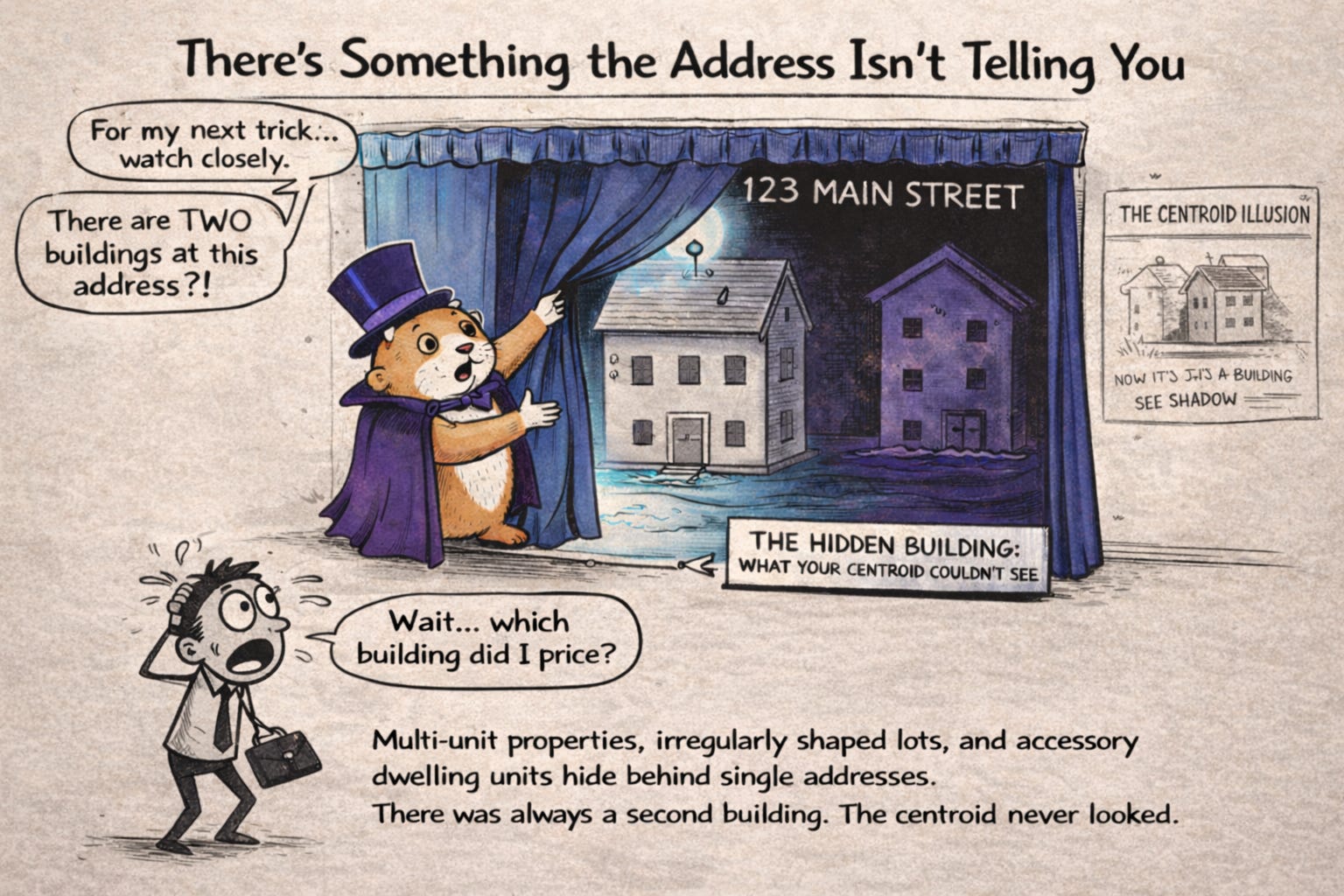

Ecopia AI has published analysis suggesting that more than one million U.S. buildings may be misclassified under parcel-centroid geocoding, representing tens of billions of dollars in potential exposure mispricing.

The shift from "good enough" location data to building-level precision reflects a hard truth the industry spent years avoiding: if your address resolution places a property in the wrong flood zone, your risk model doesn't just underperform, it becomes actively misleading.

For years, address accuracy was treated as plumbing: necessary, assumed, and rarely interrogated. Underwriting teams focused on hazard models, modifiers, and scores while quietly trusting that the address beneath them was "basically right." That assumption held when risk models were coarse. It breaks when underwriting decisions depend on structure-level signals.

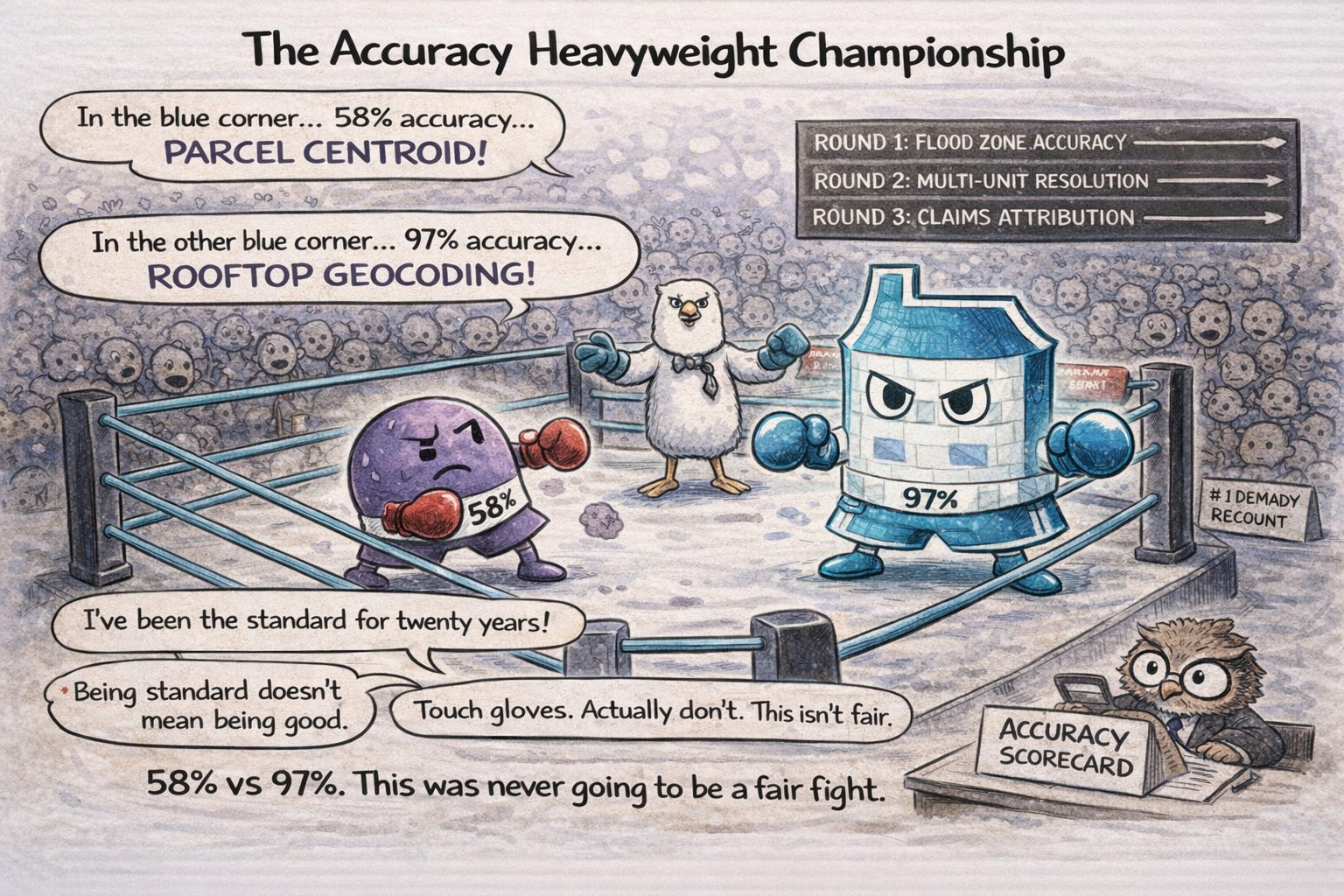

Ecopia AI's Building-Based Geocoding product has been adopted across underwriting, research, and risk analytics functions at Titan Flood Insurance (June 2025), Standard Casualty, SageSure, Openly, Farmers, Swiss Re, and Tokio Marine North America Services. It reports 97%+ building-level accuracy in independently validated tests, compared to materially lower accuracy rates typical of parcel-centroid approaches in complex parcels.

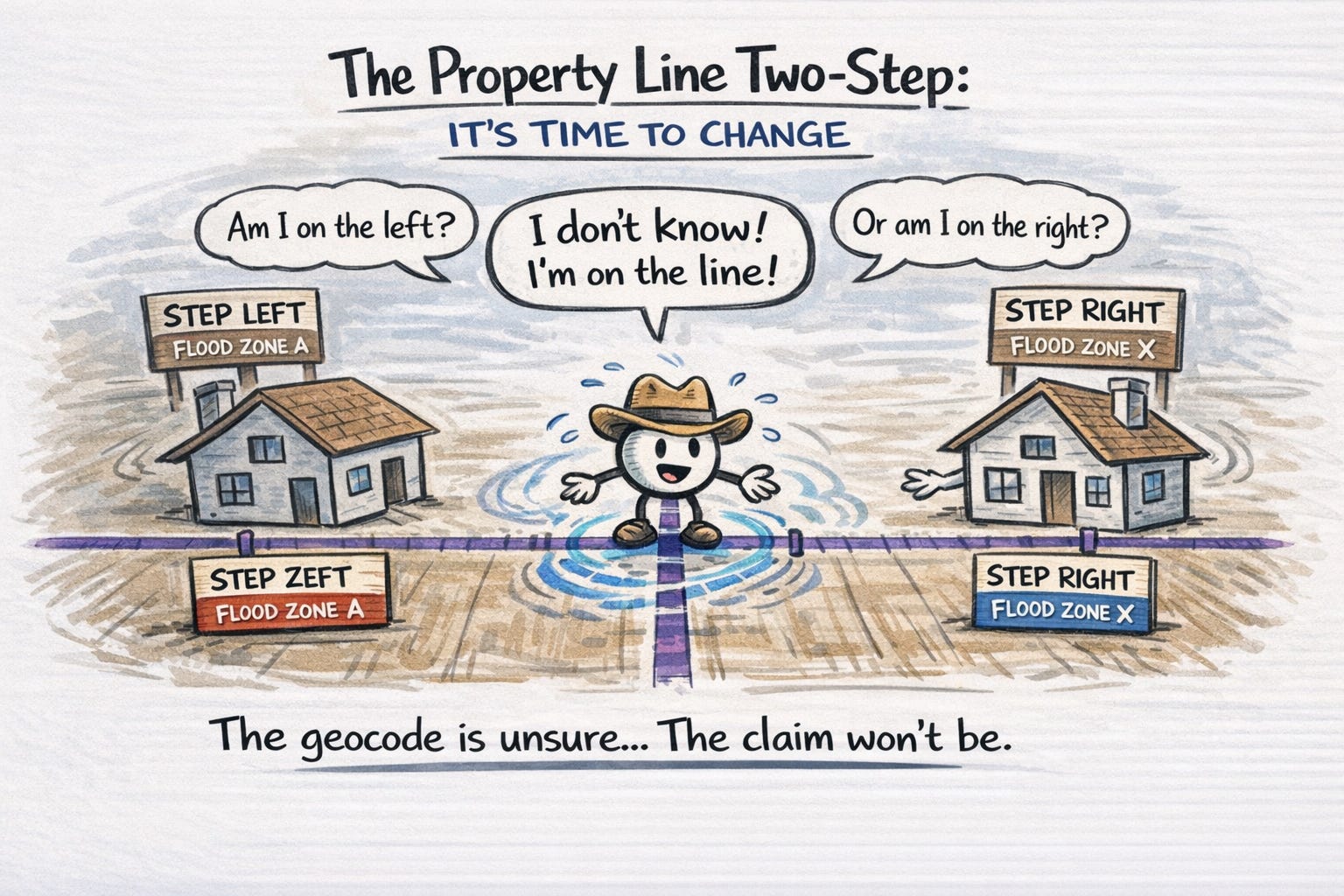

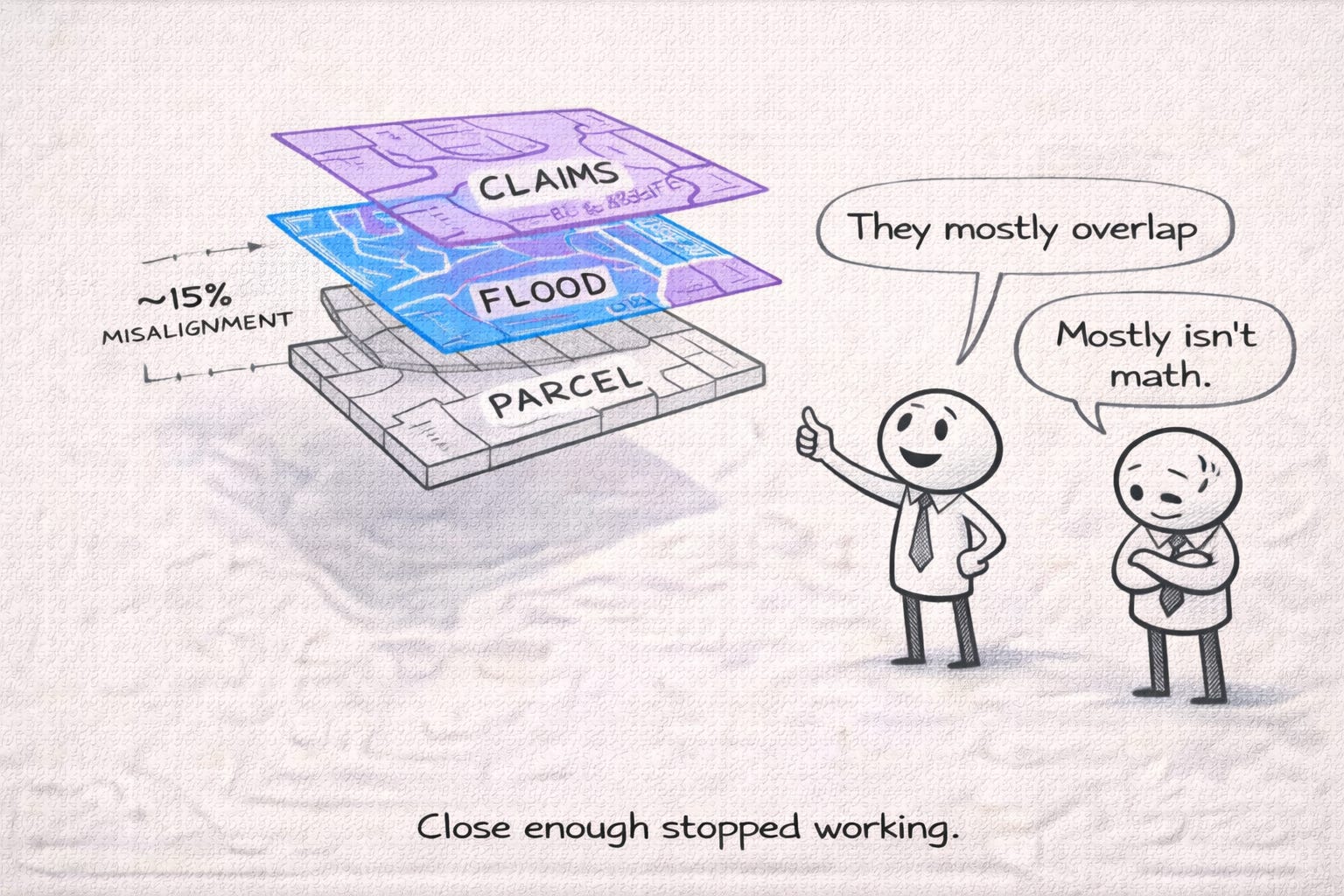

The delta matters because parcel centroids—the traditional approach—place geocodes at the mathematical center of a tax parcel, which often bears no relationship to where the actual structure sits. For irregularly shaped lots, multi-unit properties, or manufactured home communities with complex layouts, centroid-based geocoding can land you in the wrong flood zone entirely.

The uncomfortable implication is that better risk models increase the cost of bad geocoding. High-resolution inputs (roof condition, elevation, vegetation proximity, micro-topography) don't compensate for location error; they amplify it. A precise flood model mapped to the wrong structure produces confident, repeatable mispricing.

Addresscloud's April 2025 partnership with Smarty brought rooftop-level accuracy across more than 200 million U.S. addresses into their North American offering launched the prior month. CEO Mark Varley's framing was blunt: "There are over 210 million addresses in the US, but underwriters too often rely on incomplete or inaccurate information to assess these risk addresses." Following a 2025 growth investment from Kester Capital, which later closed its £425m Fund IV.

First American Data & Analytics, working from its 8.6 billion document archive covering 99% match rates (not positional accuracy) of recorded deeds and mortgages, now reports over 95% match rates to parcel data. The June 2025 partnership with Esri to make spatially-enabled parcel datasets available through ArcGIS Living Atlas opens this data to carriers already embedded in the Esri ecosystem.

The regulatory dimension matters too. Guidewire HazardHub's July 2025 partnership with Milliman Appleseed to offer the Fire Suppression Score 2.0 through a subscription service with pre-approved regulatory filings demonstrates that address-level precision has implications beyond underwriting accuracy—it affects your speed to market with new rating factors.

If building-level geocoding is demonstrably more accurate than parcel-centroid approaches, why hasn't it been the default for years?

Perfect geocoding does not exist. Multi-unit properties, rural routes, manufactured home communities, and inconsistent assessor records all introduce ambiguity. What changed in 2025 is that leading vendors began exposing that uncertainty instead of collapsing it into a single latitude–longitude. That forces a governance decision: do you prioritize speed and accept silent error propagation, or require confidence scores and fallback logic even if it slows decisioning? Neither choice is free.

The answer is cost and integration complexity. Ecopia's 178 million building footprints with 270 million+ address points, updated annually from fresh high-resolution imagery, represents a fundamentally different data architecture than traditional geocoding services that simply match an address string to a latitude-longitude pair. Addresscloud's claim of sub-200ms performance at scale when processing 300 million building footprints against 200+ flood raster files required what the company describes as "recent technological breakthroughs" to achieve.

There's also the question of who bears the cost of historical underpricing. If Ecopia's $43 billion value-at-risk figure is even directionally correct, some portion of that underpricing is already on carrier books. Correcting it means rate increases for properties that were previously misclassified, politically difficult in an environment where insurance affordability is already a regulatory flashpoint.

And the accuracy claims themselves warrant scrutiny. Ecopia's 97% figure is contractually guaranteed and independently validated, but accuracy metrics depend heavily on definition. What counts as a "match"? Over what geography? For what property types? A manufactured home community in Texas presents different challenges than a brownstone block in Brooklyn. Carriers evaluating these products should demand granular accuracy breakdowns by property type, geography, and use case rather than accepting aggregate figures.

The market is consolidating around a building-level standard, but vendors are approaching it from different directions.

Ecopia AI's strategy is vertical: own the most complete building database (178 million buildings, 270 million addresses) and append flood zone classifications, confidence scores, and year-over-year change detection. The June 2025 customer win with Titan Flood Insurance Company, an AI-powered, cloud-native flood insurer, validates that new entrants are building on building-level data from day one rather than retrofitting legacy geocoding.

Addresscloud is pursuing horizontal expansion from its UK base. The March 2025 North American product launch covered 150+ million properties with 20 natural hazards, sourcing flood data from JBA Risk Management and wildfire insights from Precisely. The October 2025 partnership with Artificial Labs integrates Addresscloud's geocoding directly into algorithmic underwriting workflows, "at the point of underwriting," as Varley put it, rather than as a lookup layer.

First American Data & Analytics leverages its 135-year title heritage and 8.6 billion document archive to provide parcel data with over 95% match rates. The June 2025 Esri integration and April 2025 VeriTitle launch (detecting liens and ownership issues at application) suggest First American sees address intelligence as one element of a broader property lifecycle platform.

ATTOM's August 2025 launch of ATTOM Nexus, a self-service platform for property data evaluation, and the July 2025 Snowflake integration reflect a different bet: making property data more accessible through modern cloud infrastructure rather than competing on geocoding precision specifically. ATTOM's unique ID system linking 158 million properties provides entity resolution, but the core geocoding capabilities remain less differentiated.

Nearmap's October 2025 launch of Roof Age Gen2, claiming 95% accuracy across 151 million US parcels using multi-source data fusion, demonstrates that aerial imagery providers are also embedding address accuracy into their products. The pre-processing for sub-2-second delivery suggests an API-first architecture designed for real-time underwriting integration.

First, quantify your current geocoding accuracy by property type and geography. Ask your existing vendors for accuracy breakdowns—not aggregate percentages, but performance by manufactured homes, multi-unit properties, rural versus urban, and flood zone edge cases. If they can't provide this granularity, that's a data point.

Second, request flood zone discrepancy analysis. Ecopia's methodology specifically identifies buildings where parcel-centroid geocoding places properties outside flood zones when building footprints actually fall inside. Ask any vendor you're evaluating to run this analysis against a sample of your portfolio. The results will tell you whether building-level geocoding is a nice-to-have or a pricing imperative for your book.

Third, evaluate confidence scores. Both Ecopia and First American append confidence metrics to their geocodes. These scores enable straight-through processing for high-confidence matches while flagging ambiguous locations for review. If your current workflow treats all geocodes as equally reliable, you're likely over-inspecting some properties and under-scrutinizing others.

Fourth, check integration architecture. Addresscloud's sub-200ms API response times and Ecopia's pre-appended FEMA flood zone classifications reduce the number of sequential API calls required in underwriting workflows. For high-volume operations, milliseconds compound into operational cost.

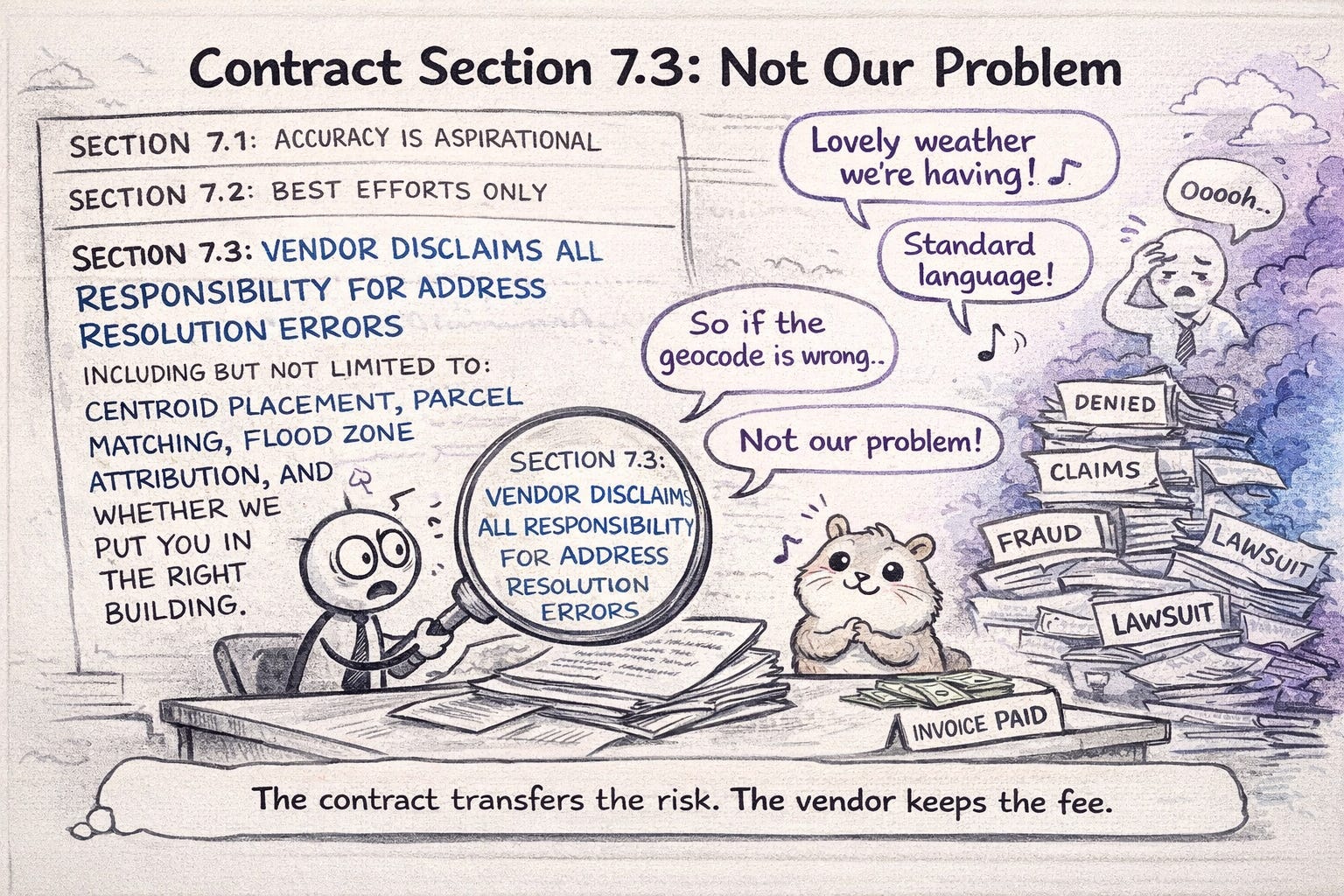

Fifth, negotiate accuracy guarantees contractually and review contracts for silent failure. Many data agreements disclaim responsibility for address resolution errors while still powering underwriting and rating decisions. That mismatch mattered less when models were coarse. It matters now. If a vendor won't commit to accuracy definitions, confidence thresholds, and remediation when errors surface, ask where that risk is expected to sit—because it won't disappear.

Address-level accuracy moved from a data quality checkbox to a competitive differentiator in 2025. The vendors that can prove building-level precision with confidence scores and regulatory-ready integrations are pulling ahead; those still relying on parcel centroids are accumulating mispriced risk. For CUOs writing hail and wind business, where claims attribution depends on knowing exactly which structure was hit, this is no longer optional infrastructure.

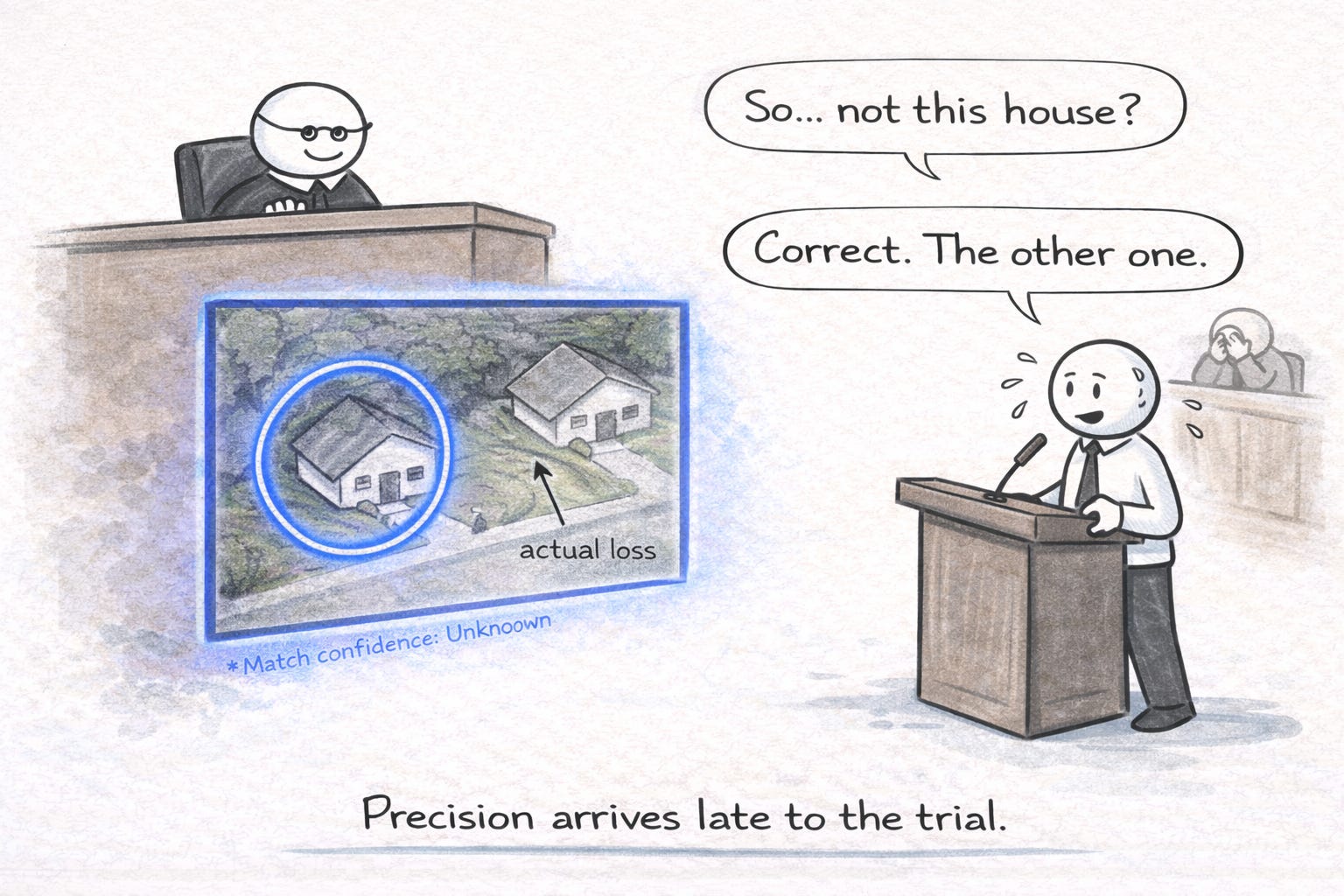

If your address resolution is off by one parcel, your entire risk model collapses.

3 min read

I recently had the opportunity to present to several dozen agents for the PIA Western Alliance last week. The title of my presentation was: ”Wildfire...

5 min read

Welcome to our inaugural issue of The Property Intelligence Report, where we explore the latest developments in property intelligence technologies...

4 min read

Fear in the Insurance Jungle – the Condo Policy by Patrick Kelahan Not many speak of the elephant in the insurance room, even though there are...