.jpg) Nicholas Lamparelli

Nicholas Lamparelli

5 min read

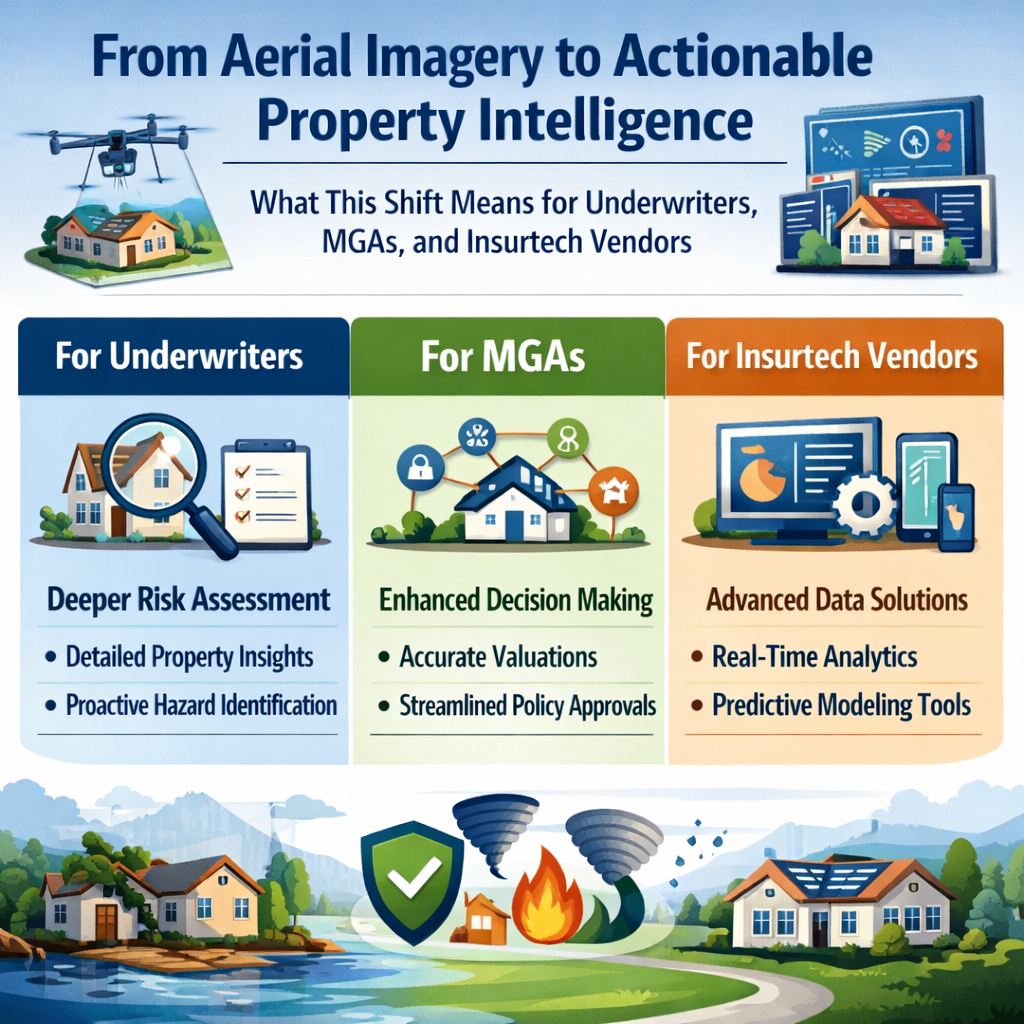

The Property Intelligence Report: Aerial Imagery Deep Dive

Welcome to our inaugural issue of The Property Intelligence Report, where we explore the latest developments in property intelligence technologies...

5 min read

Welcome to our inaugural issue of The Property Intelligence Report, where we explore the latest developments in property intelligence technologies...

3 min read

I recently had the opportunity to present to several dozen agents for the PIA Western Alliance last week. The title of my presentation was: ”Wildfire...

3 min read

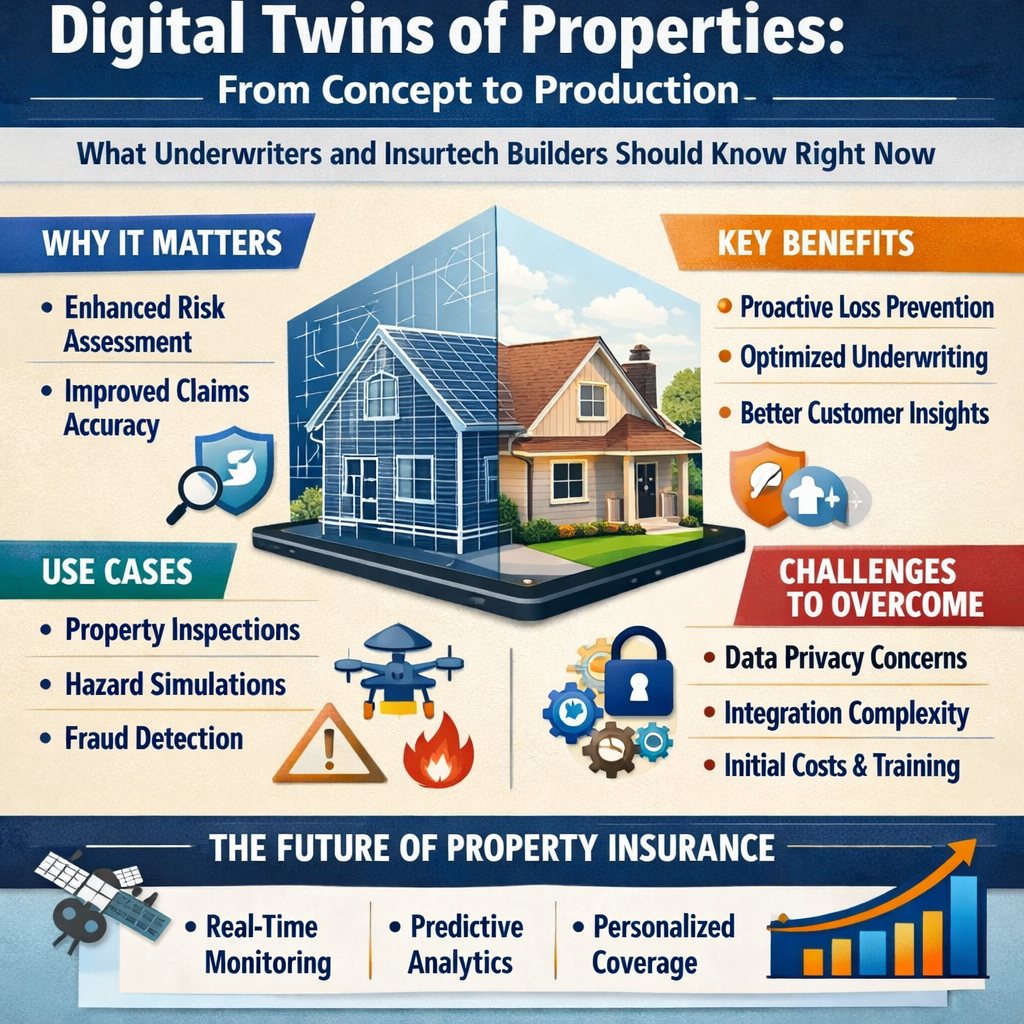

Property digital twins have quietly moved past the proof-of-concept stage, and the implications for underwriting, claims, and portfolio management...