.jpg) Nicholas Lamparelli

Nicholas Lamparelli

2 min read

Insurance AI's Success Now Depends More on Operations Than Algorithms

The hardest part of insurance AI isn't building the models anymore, it's making them work reliably within the messy realities of legacy systems and...

2 min read

The hardest part of insurance AI isn't building the models anymore, it's making them work reliably within the messy realities of legacy systems and...

1 min read

PIR 188 Conversation with Cole Winans, CEO of Flyreel about AI and InsurTech by Antonio Canas Video version: Audio version: ...

3 min read

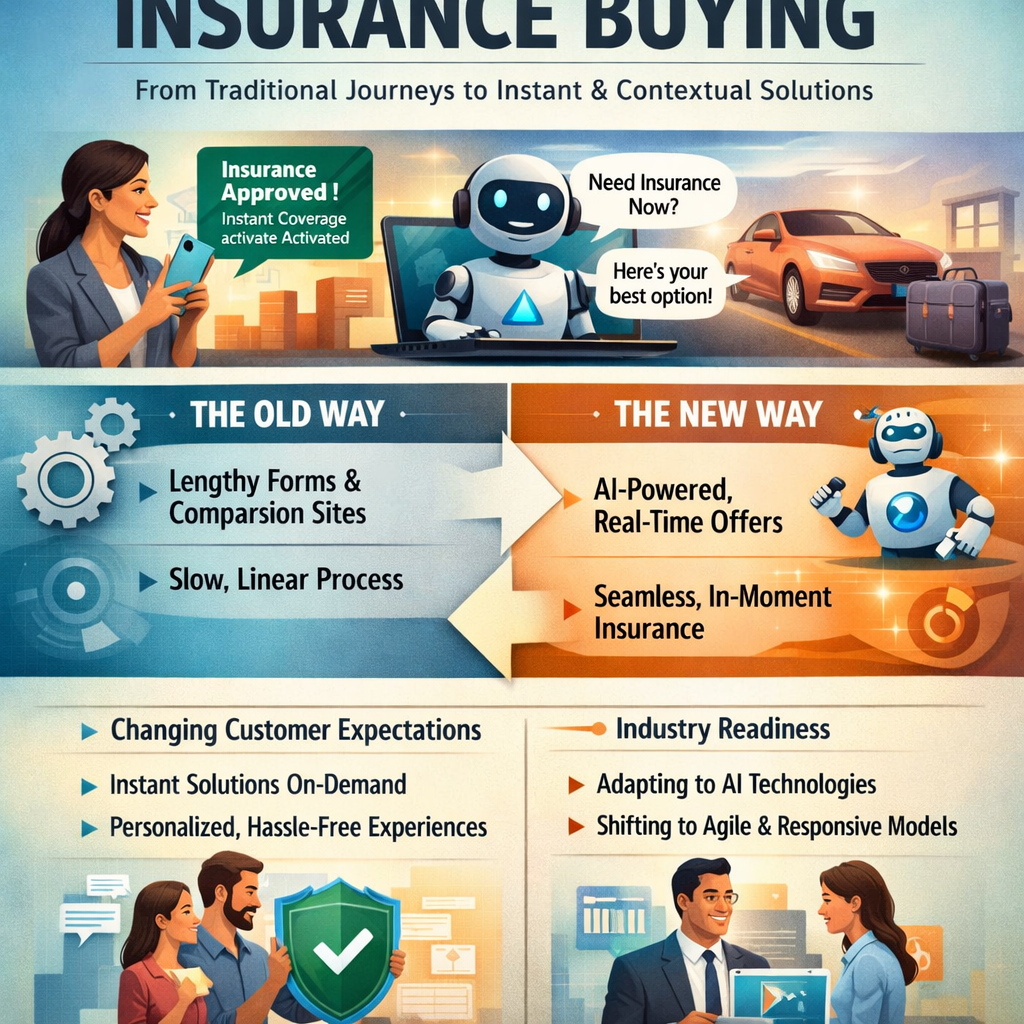

The insurance industry has spent years talking about digital distribution. Websites were the first step. Then came embedded experiences, self-service...