In an insurance company’s intricate corporate architecture, the team responsible for exposure or aggregate management is vital to maintaining financial stability and ensuring the company is not overly exposed to a loss event that would prevent it from meeting its obligations. This team’s primary role is to monitor and manage the accumulation of risk across the company’s portfolio, helping to avoid overexposure to potential losses. Determining where this team should be positioned within the organizational structure is a crucial decision that can significantly impact the company’s risk management effectiveness.

Several departments could potentially house the exposure and aggregate management team, each offering distinct advantages:

- Catastrophe Modeling Team:

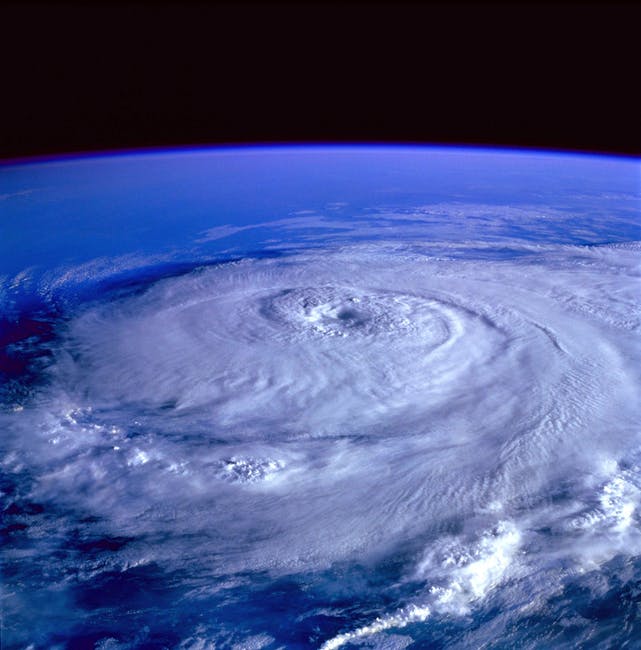

Catastrophe modelers focus on quantifying potential losses from large-scale events. Since forecast losses are highly correlated with aggregate exposure, it makes sense that the modeling team compile both statistics. By integrating exposure management, the company benefits from a more comprehensive view of its risk landscape, leading to more accurate risk assessments and enhanced strategies for managing aggregate exposures.

- Enterprise Risk Management (ERM):

Incorporating exposure management into the broader ERM framework provides a holistic approach to risk oversight. ERM teams typically have a broad view of the company’s risk profile, including operational, financial, and strategic risks. By situating exposure management within this context, companies can ensure that aggregate risk is considered alongside other critical risk factors, enabling more balanced and informed decision-making.

- Ceded Reinsurance Team:

The ceded reinsurance department is responsible for transferring risk to reinsurers, making it a natural fit for exposure management. Aligning these functions allows the company to optimize its reinsurance strategy based on a thorough understanding of its aggregate exposures, leading to more efficient risk transfer and potentially reducing costs associated with reinsurance purchases.

- Underwriting Team:

Integrating exposure management into the underwriting department provides immediate feedback on how individual policy decisions impact the company’s overall risk profile. This real-time insight helps underwriters make more informed decisions about risk selection and pricing, ultimately leading to a more balanced and profitable portfolio.

- Actuarial Team:

The actuarial department’s focus on quantitative analysis and risk modeling makes it another potential home for exposure management. Actuaries are skilled in assessing the long-term financial implications of risk, which aligns well with exposure management’s goals. This integration could lead to more sophisticated pricing models and reserve calculations that account for aggregate risk.

- Claims Team:

Placing the exposure management team within the claims department can provide valuable insights into the practical implications of risk assessments. The claims team deals directly with the outcomes of risk events, offering real-world data that can refine exposure models and strategies. This integration ensures that exposure management is grounded in the realities of claims experience, enhancing the accuracy and relevance of risk assessments.

Each of these placements offers unique benefits and potential challenges. The optimal location for the exposure and aggregate management team depends on factors such as the company’s size, structure, and strategic priorities. Regardless of where it sits in the organization, the exposure management team must maintain strong communication lines with other departments. Cross-functional collaboration is essential for effective risk management, as exposure-related insights can inform organizational decision-making.

Some insurance companies choose to create a standalone exposure management department that reports directly to senior leadership. This approach ensures that exposure considerations are given appropriate weight in strategic decisions and that the team has the independence to provide objective assessments.

Ultimately, the goal is to position the exposure and aggregate management team to maximize its impact on the company’s risk management practices. This may involve a hybrid approach, where the team has strong ties to multiple departments or where team members are embedded across different functions. As the insurance landscape evolves, companies must remain flexible in their organizational structures, regularly evaluating the exposure management team’s placement and effectiveness to effectively navigate an increasingly complex risk environment.

About Peter Crowe

Peter Crowe began his career in technology consulting, which led him to many cities, companies, and even a few countries doing system implementations, upgrades, and conversions. A tech project he worked on led to an opportunity at RE/MAX, a real estate franchise company. Pete joined RE/MAX in 2013 and while there, served in various capacities including Vice President of Investor and Public Relations, Sr. Vice President of Marketing, Communications, and Investor Relations, and Executive Vice President of Business and Product Strategy.

Pete joined We Insure, a PEAK6 InsurTech company, in September 2019, where he served in the roles of Chief Revenue Officer and Service Operations lead. In these roles, Pete partnered with leadership and the We Insure team to help make We Insure an unstoppable force in the insurance industry. Through strong strategies and partnerships, Pete was able to assist in the expansion of We Insure into 25 new states, growing the agency footprint from 90 to 190 offices in just over two years.

In 2021, Pete shifted to the role of Executive Vice President of Team Focus Insurance Group, another PEAK6 InsurTech company, and has served as President of Team Focus for two years.

Pete holds a Bachelor of Business Administration from Indiana University, and an MBA from the University of Denver – Daniels College of Business.

Nick Lamparelli is a 20+ year veteran of the insurance wars. He has a unique vantage point on the insurance industry. From selling home & auto insurance, helping companies with commercial insurance, to being an underwriter with an excess & surplus lines wholesaler to catastrophe modeling Nick has wide experience in the industry. Over past 10 years, Nick has been focused on the insurance analytics of natural catastrophes and big data. Nick serves as our Chief Evangelist.