If you work in insurance, chances are that you’re attached somehow to one of the big players in the market. You will likely be putting a lot of effort into making sure that not only does your firm remain one of the big players, but that it finds new ways to grow and keep pace with its rivals.

What you also may have noticed is that big business is increasingly staring enviously at small start up fintech firms for inspiration and collaboration. They want to make sure that when the much promised ‘fintech revolution’ happens, they are not left behind.

We’ve all read about what happened to Kodak or Blockbuster Video when they failed to get on board with the tide of disruption when it washed over their industries.

However, one of the things that has puzzled me is why these huge businesses, with seemingly-unlimited resources, are looking at these tiny firms to show them the way forward?

Lemonade is the darling of the insurance world right now, and although their very recent market growth is impressive, they, like several other of their start up brethren, have been the subject of finger pointing, link sharing and gasping amongst insurance execs for the past few years. This is even before they started making money.

But why?

What is it that makes big firms envious of what these smaller firms are doing, or even proposing to do?

I’m lucky that a lot of what I do in my day job is examining this very question – how can we, as a big firm, capture some of that ‘start-up lightning in a bottle’ and use it to supercharge our business. I’ve had a go at trying to dissect (in a brief a way as possible) what I think it is that makes the difference, and why were all looking at Lemonade rather than Lloyds to show us the way forward.

Internal Factors

To start with, I’m going to take a look at three things that are all within the control of insurers internally that might be hindering or inhibiting innovation:

1. We’re too “insurancy”

Not only have I made this word up, but this might seem like a ridiculous thing to say, right? How can insurance people be the wrong type of people to help solve the insurance problems we’ll all be facing in the years ahead?

Well, I hope you’ll see it might be truer than you first think.

If you work in a big insurance organisation, you’ll be aware that the gears of change and innovation are huge, heavy, and have been in place for many, many years. To create something new and exciting, it needs to be passed through each of these gears, checked and double checked at each stage to make sure what you’re proposing is sound and good for the business

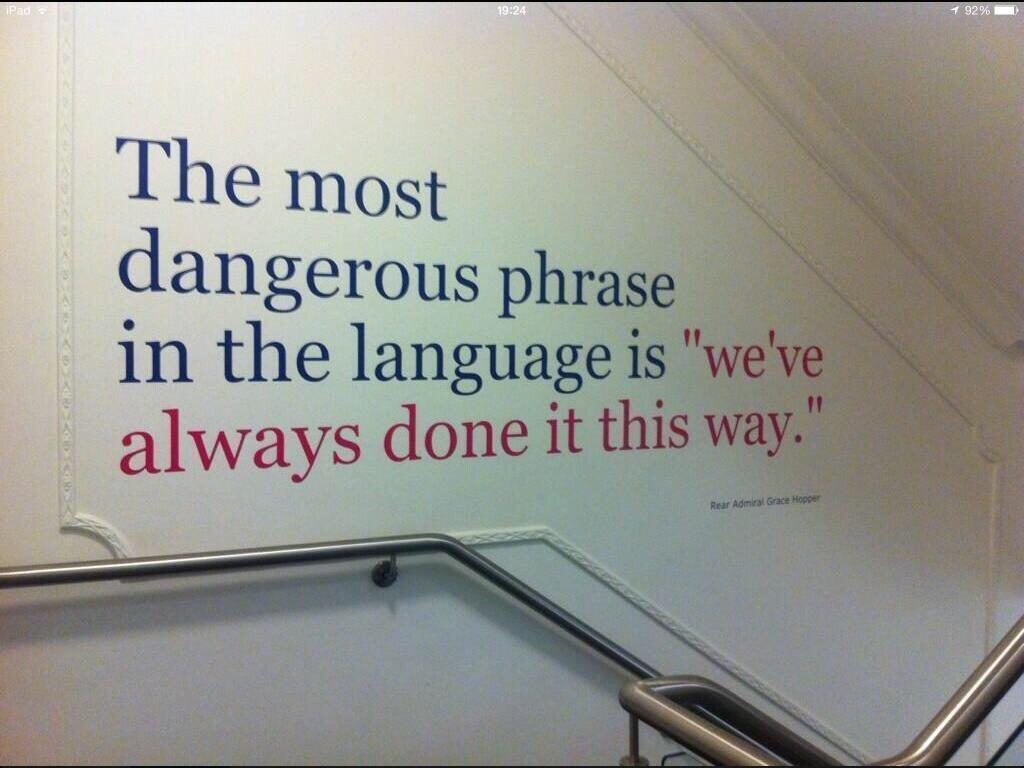

Checking ideas thoroughly before you unleash them on the world is in principle a great idea. However, each one of the ‘gears’ in this scenario is an insurance person – and most insurance people think and live and breathe insurance, and specifically “the way is always been done.”

This can seriously stifle our ability to create something really game-changing.

The reason why some of these start-ups are creating things so new and exciting is because they’re not tackling the problems that tomorrow’s insurance needs to solve using today’s insurance rules as a template.

If, when Apple decided to make a phone, they made sure it ‘fell into line’ with all of the criteria that other hugely popular telephone manufacturers like Nokia were using, would we have got the iPhone? I think not.

One of the main reasons we got something so different is that they approached creating a phone like a software firm would: they changed the game by thinking differently, and coloured outside the lines of what other firms were doing to fundamentally change the landscape of how phones are made and used.

This is what start-up firms are doing – they’re not approaching insurance thinking like insurers; they’re approaching it thinking like a software firm or an ecommerce firm, and as a result are creating insurance products and interfaces which are truly different.

Take Trov as a great example. they are thinking inventory first, gamification second, and oh, there’s insurance third if you need it. This isn’t the way any big insurer would approach a developing new acquisition channel, however Trov’s eye-watering year-one numbers shows that they were onto something, despite it being something that the big boys wouldn’t have even contemplated.

With that in mind, I feel that lesson one is;

To create things which look and feel fundamentally different, rather than more of the same with a shiny coat of paint, insurers need to engage with people from outside of the industry; have a fresh pair of (non-insurance) eyes look at the problem; and work at developing solutions that insurance people won’t have considered.

2. We’re afraid of failure

Now we need to take a closer look at those huge ‘gears’ of change that seem to be in place at the majority of insurance firms.

Now, as I’ve already mentioned, a robust change programme is a fantastic thing to reduce the risk of going to market with something that isn’t right, or isn’t ready (or both). But can being so risk-averse actually harm an insurer’s chances of doing something transformational?

There are a litany of famous phrases, passages in books about innovation and lessons from brave firms across various industrial sectors that teach us failure is an absolutely essential part of the process of learning and, ultimately, building something great.

Start ups get their ideas together and out to market fast. They’d rather learn their lessons around whether something works or not in the real world than spending hours chewing over the ‘what if’s’ and ‘maybe’s’ around a table, before drawing up a detailed 9 month action plan.

The latter, however, is where a lot of big insurers find themselves when it comes to doing something new. Internal change processes and procedures can inhibit innovation.

Often, by the time an insurer has gone through every step in their internal change process to get something out to market, a start-up has launched numerous iterations of a similar product and are much closer to nailing a great proposition that people want.

I will caveat this with one small ‘but’, as insurers (particularly large ones with lots of history and lots of customers) will obviously need to consider potential damage done to their brand by going to market with something too crazy. However, if insurers have good, creative people on board and a clear idea of what they want to achieve with some clear guidelines OK’d by senior management, they’ll be surprised at how being seen as innovative and unafraid to try new things will boost, rather than damage, a brands image.

So, with all of that as it is, my second lesson for the big boys would have to be:

To make sure that new propositions are both the first of their kind in the market and ones that people will love, insurers must stop worrying about failure, and move projects focused on disruption and innovation outside of their existing change processes. Embrace live testing and the failure that it brings as an essential part of making something that people want to engage with.

3. Our systems are enormous

The size of our organisations often pose as barriers when it comes to innovation which simply are not there when start up firms are tackling similar problems. I’ve already mentioned this when looking at internal change programmes above, and with just a mild fear of repeating myself, want to shift the focus slightly to look at huge internal IT systems and how these can hinder rather than help insurers innovate.

Those working for large insurers will know that internal IT systems are, although sometimes quite nuanced to navigate, great at enabling customers to buy or change their insurance policies, or to handle claims when bad things happen.

However, the issue with innovation, and particularly getting a pilot or a test version of a new proposition out in the market, can sometimes be “how are we going to plug in this new shiny thing that we’re building to our existing legacy IT infrastructure?”

For insurers this can be a real quandary, as quote and pricing engines and customer databases are often ‘hard baked’ into existing systems, and they want this functionality (or at least a part of it) to be included in whatever it is they’re launching; however to do so is not only mind-bendingly complicated, but is also extremely costly.

Start ups aren’t wrestling with the same issue – they don’t have to worry about somehow linking up the new front end with their old back end as they’re starting from scratch. As a result they can go to market right away without all of the head scratching and huge amount of time, effort and money to get it to work.

So what’s the answer for insurers?

In my opinion, during the innovation phase not everything needs to work perfectly, and, where possible, insurers should look to ‘hand crank things’ behind the scenes that might be automated in a finished product to save time, effort and money in developing.

If insurers are prepared to present something to customers that demonstrates the core idea without 100% of the functionality of the finished article, they’d be able to get to market faster and at a fraction of the cost.

U.K. Firm brolly is a great example of this – they’ve gone to market with a system that they’re still playing with, however the key thing is that they’ve gone to market! They’re making customers aware that things aren’t quite finished, but are still able to articulate what they’re looking to do and why customers will love it.

This approach, essentially using a start-up mind-set and not concerning themselves with the legacy systems already in place, would quickly give insurers the chance to know whether their idea actually works in the real world, and what ‘tweaks’ they need to make to create something really compelling, before investing enormous amounts of time and money into an integrated solution.

So lesson number three;

Insurers should take pilot propositions to market before thinking through every minute detail of how system integration might work. Fake what you can to learn what people really want, and worry about the scalability and IT spaghetti once you know exactly what people like, and what it is you’re going to build.

***

So that is it for part one!

In part two, I’ll be examining some of the external factors that can affect why big insurers struggle to innovate in the same way as start ups, and what they might be able to do to tackle them

About Nick Reed

Nick Reed is an insurance professional from the south east of England, with a passion for fintech and the future of the industry. He has over a decade of insurance business experience working across numerous sectors, and is currently developing new products for a FTSE 250 UK based insurer. He currently lives and works in Kent, and writes his own blog at insurancebluster.com

Nick Reed is an insurance professional from the south east of England, with a passion for fintech and the future of the industry.

He has over a decade of insurance business experience working across numerous sectors, and is currently developing new products for a FTSE 250 UK based insurer.

He currently lives and works in Kent, and writes his own blog at insurancebluster.com